The demise of Wirecard and the scope of its alleged malfeasance are compelling all players in the payments space—merchants, acquirers, scheme operators, and rising fintech providers and investors—to undertake a review of their payment strategies and take actions to mitigate current and future risks.

The demise of Wirecard and the scope of its alleged malfeasance are compelling all players in the payments space—merchants, acquirers, scheme operators, and rising fintech providers and investors—to undertake a review of their payment strategies and take actions to mitigate current and future risks.

This research note highlights two factors that impact any change in a payment provider and are part of a larger concept called Payment Orchestration.

Key Issues

- What are the long-term implications of the Wirecard debacle?

- What are the emerging payments strategies?

- How realistic is it to change payment providers?

- What are best practices for global payments?

- Who are the winners and losers in payments and commerce?

Background

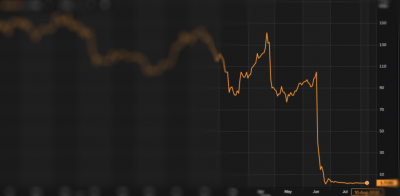

Sudden economic downturns often bring to the surface accounting and financial skullduggery that is hidden by a booming economy. When the COVID-19 pandemic hit earlier this year, historically minded journalists went into high gear, scanning the horizon to see which creative accounting scandal would rise to the waterline first. They didn’t have to look far. Since June 18th, the survival of Wirecard AG, one of Europe’s largest payments companies, a one-time rival to SAP, and Germany’s fintech darling member of the DAX 30, is in doubt. Like past events, this one may pull related parties down and likely result in regulatory and industry changes that affect everyone in the payments industry for years to come.